Call Options: A Practical Guide for Real Estate Investors

Explains what call options are, how they work, and why traders use them to gain upside exposure with defined risk.

Tags

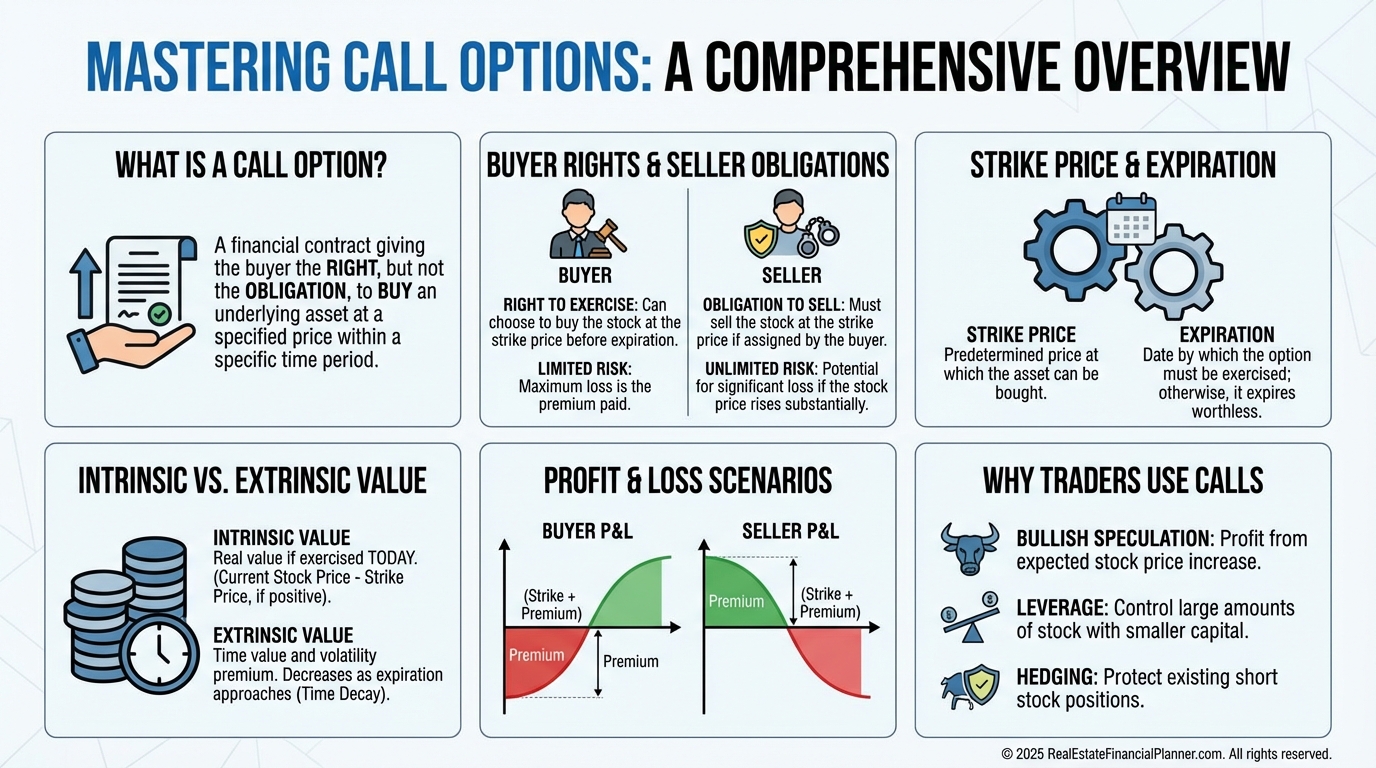

A call option gives you the right, but not the obligation, to buy a stock at a specific price (the strike price) on or before a specific date (the expiration). You pay a premium for that right, and that premium is the maximum amount you can lose as the buyer of a call.

Call options are used when you believe a stock’s price will rise. If the stock moves above the strike price before expiration, the call option gains value. If it does not, the option expires worthless, and your loss is limited to the premium you paid.

Each call option controls 100 shares of the underlying stock. This creates leverage. You can gain exposure to the upside of a stock with far less capital than buying the shares outright, but that leverage cuts both ways. Options lose value over time due to time decay, which accelerates as expiration approaches.

A call option’s price is made up of two parts. Intrinsic value is the amount the option is in the money, if any. Extrinsic value is everything else, including time value and implied volatility. Even if the stock moves up, changes in time and volatility can still impact the option’s price.

Traders commonly use call options to speculate on upside moves, replace stock positions with less capital, or express bullish views with defined risk. The key tradeoff is simple: limited downside in exchange for a limited window of time for the trade to work.

Understanding call options is foundational. Once you grasp how strike price, expiration, time decay, and leverage interact, you can decide when calls make sense—and when owning the stock or using a different strategy is the better move.